A través de este acuerdo, Aon y Finnovating buscan seguir impulsando la innovación y potenciar…

Finnovating’s success at Frankfurt Digital Finance

Rodrigo García De La Cruz, CEO of Finnovating, was a shining star at the recent Frankfurt Digital Finance Conference. As one of only two Spaniards in attendance, Rodrigo stood out and made a lasting impression, particularly when he was interviewed by the General Director of the Central Banking Association. His knowledge and passion for innovation in the financial sector were evident, and it quickly became clear why he and his company, Finnovating, were the highlight of the event.

Frankfurt, being the financial engine of Europe, were the perfect setting for Rodrigo to showcase the success of Finnovating. With a truly global perspective and deep insights into the Latin American market, Rodrigo’s vision for the future of finance has already garnered much attention and accolades. His innovative platform, which connects thousands of financial institutions with over 50,000 FinTech solutions, has already facilitated over 1,000 collaborations in just 18 months. It’s no wonder why Finnovating is already a household name in the industry.

🚀 Would you like to publish your own event and invite the most innovative leaders and startups of the ecosystem? Post it now in the Finnovating platform.

The attendance of the Rodrigo at the conference was important for several reasons. Firstly, the conference is one of the largest and most influential gatherings of financial industry professionals and stakeholders, and attending it provides an opportunity to network with other leaders and decision-makers in the field. Secondly, Frankfurt is one of the major financial centers in Europe and his presence at the conference demonstrates Finnovating’s commitment to playing a role in shaping the future of digital finance in the region and the world.

Additionally, attending the conference provides the platform with an opportunity to learn about the latest developments and trends in digital finance, including emerging technologies and innovative business models. This will help us to make informed decisions about how to position the platform for growth and success in the rapidly evolving financial landscape.

Sarah Schmidtke (moderator) is a prominent figure in the financial industry and is associated with the Interessengemeinschaft Frankfurter Kreditinstitute (IFK) and the Central Banking Association. She is known for her deep understanding of the banking sector and has been actively involved in the growth and development of the financial industry. With her extensive experience, Sarah has been able to provide valuable insights and solutions to the banking sector and has played a key role in shaping the future of the industry. Her dedication and commitment to her work have made her the perfect person to moderate the panel Finnovating was in, providing a key point of view while speaking with Rodrigo García de la Cruz.

Interview of Rodrigo García De La Cruz at Frankfurt Digital Finance

SS (Sarah Schmidtke): Can you share with us your personal experiences of developments and failures in the FinTech sector as an entrepreneur, investor, influencer and academic professional with over ten years of experience? Why did you feel the need to create Finnovating, a platform that connects and matches business opportunities between, for example, a bank and a FinTech company?

RDLC (Rodrigo García De La Cruz): My personal experiences with the FinTech sector have been greatly impacted by the pandemic. Prior to the pandemic, I noticed that banks were disconnected from FinTech and saw them as a competitor or lacking value. Banks used to work in a «do it yourself» format, developing digitalization and innovation internally with their own resources. Most Tier 1 banks created innovation areas as a trendy space to identify trends and it often ended as showrooms for entrepreneurs, trying to integrate some of those fancy FinTech through unending proof of concepts. However, it didn’t work as banks were not prepared and FinTech were not the right size to do it well.

However, after the pandemic, there was a substantial increase in collaboration between companies, with a growth rate of five times during the pandemic and expected to increase 27 times by 2025. This is not limited to only the top banks and insurance companies, but it is mandatory for every single company in the world to accelerate their digital transformation. Banks realized that they need to speed up their transformation but focus on efficiency, UX, and their profit and loss, providing services that clients are looking for after the pandemic.

On the other hand, FinTech has become more mature and open to collaboration. Today, two out of three FinTech have B2B, SaaS, and embedded finance business models, all open to collaborate. The solution was to change from the «do it yourself» format to a «collaborative format,» as banks understand that the only way to achieve their goals is by collaborating and investing in FinTech solutions.

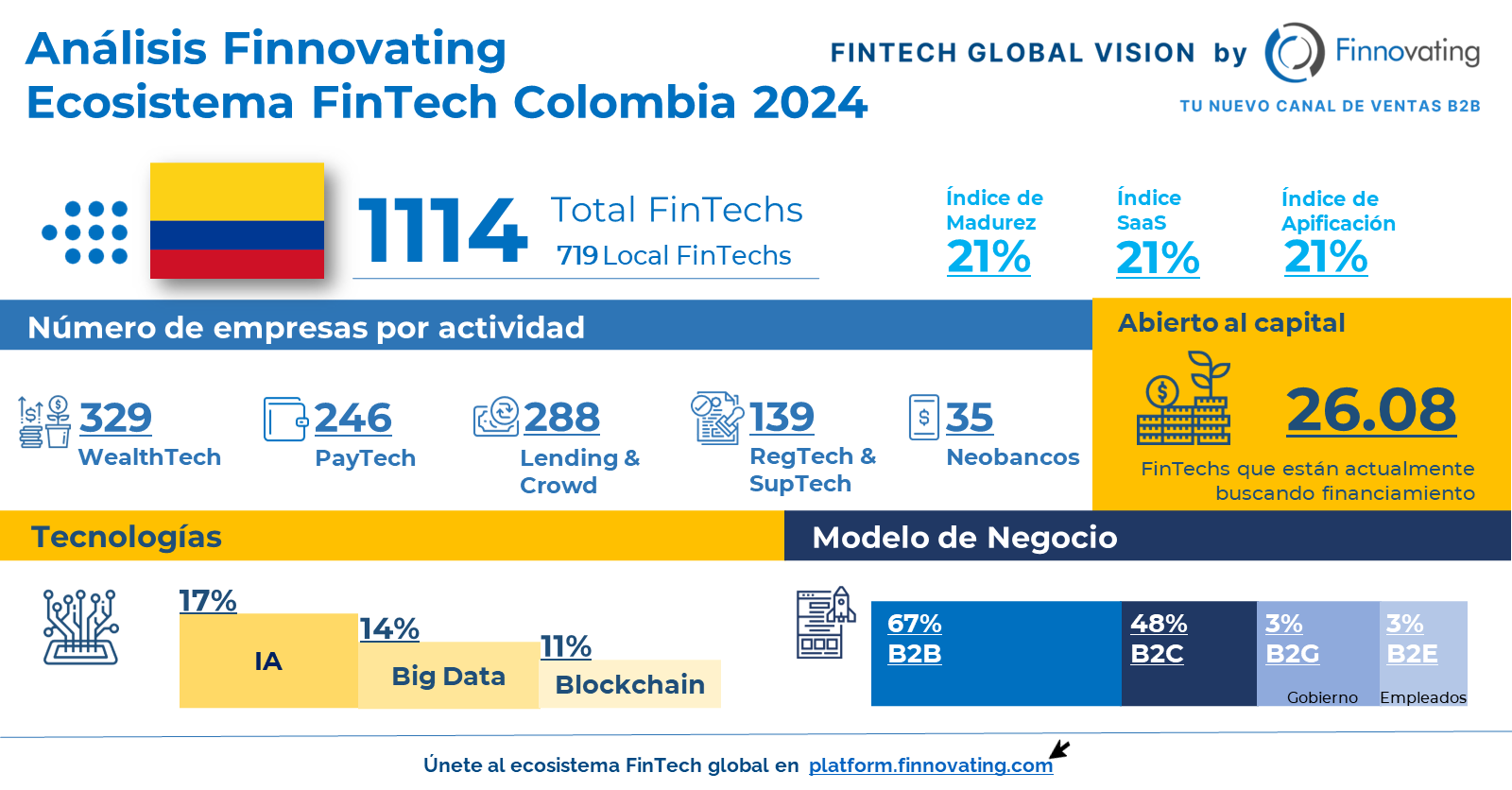

However, there was another challenge for banks. Once they knew they needed open solutions, they had to find them in a very complex and ever-changing FinTech sector, with more than 50,000 FinTech and InsurTech solutions with more than 500 different activities. After connecting FinTech with banks for 10 years and seeing all sorts of failures, I realized that I needed to change the way I connected the dots. I asked myself, «If professionals connect on LinkedIn, why can’t we create a B2B platform to connect the FinTech innovation solutions with corporations in a new revolutionary way?»

And that’s how Finnovating became the first open platform to connect the innovation in the financial industry. It solved three issues: classifying the whole ecosystem, connecting them, and doing business. We classified the 50,000 startups and scale-ups and the 500+ different activities, connecting them to the platform, and they are responsible for updating their own data with our validation. We created spaces for launching open calls or partnership challenges for collaboration and investment, reinvigorating the way to find and collaborate with the entire innovation ecosystem.

After 18 months, we have registered 25% of the whole FinTech market from 125 countries and helped banks and insurance companies create 12 million interactions between the ecosystem last year. This would not have been possible without the Finnovating platform.

SS: Finnovating connects companies from 125 countries, giving you a global view of what’s happening. You also founded the IberoAmerican FinTech Alliance, which provides deep insight into the Latam market. Taking your international perspective, which innovation trends do you see and what are the key drivers for success?

RDLC: Starting with success, I would say that there are three key drivers:

- You really want to do it, if not you will be spending time and resources just on marketing.

- Connecting innovation with business units to impact efficiency, user experience, and new digital business.

- Banks that connect business units with open innovation teams are multiplying the impact of FinTech and creating more sustainable business models for their banks.

The problem is how to do it in a tier 2 bank without the resources or budget of a tier 1 bank. And this is where the platform we have created is democratizing open innovation and collaboration, connecting all 50,000 FinTech solutions in the world and giving them the opportunity to search, find, select, and collaborate with the best tech partners to accelerate their digital transformation.

This is what is happening in the Latam region, with thousands of tier 2 banks using the platform as an open window to connect and find and integrate solutions. After 18 months, we have been able to close 1,000 collaborations between banks and tech solutions and the trends are interesting.

The top 5 FinTech solutions most integrated by banks in 2022 were:

- Embedded finance and open banking solutions.

- Lending (like Buy Now Pay Later).

- Wealth management (micro-savings and roboadvisors 2.0).

- Advanced solutions for credit scoring and fraud detection.

! Click here for more information

We are tracking all interactions on the platform, and after 12 million last year, we can see the trends for 2023:

- Sustainability-impacting solutions (we have identified more than 5,000 startups impacting sustainability).

- AI as a Service, with solutions like ChatGPT.

- Embedded finance and insurance solutions.

With regards to funding, investment in FinTech has changed in 2022, going from 140 to 88 billion (a reduction of 40%) but still double the amount of 2021. B2C companies are suffering and lending-based companies even more. However, B2B and SaaS solutions have a great future as they are able to manage finance based on their clients rather than external investors. The distribution of investment in the world is led by the USA with 50%, followed by Europe with 25% and Asia with 17%.

The problem is the number of unicorns in rounds C and D. With more than 25 million, most FinTech look to the United States to raise money and the companies end up in American hands.

Finnovating’s shining performance at Frankfurt Digital Finance

Ultimately, the attendance of the Rodrigo García De La Cruz at the Frankfurt Digital Finance Conference was an important step in establishing the company as a thought leader and player in the digital finance space. Rodrigo’s insights on the developments and failures in the FinTech sector, as well as his solution to connect banks and FinTech through the platform, Finnovating, highlights the importance of collaboration and innovation in the financial industry. With over 1,000 collaborations between banks and tech solutions closed after 18 months, Finnovating is a testament to the potential for success in the FinTech sector.

Entradas relacionadas

Esta entrada tiene 0 comentarios